ORIENT Macro — a Systematic Asian ETF Strategy | One Altitude Capital

ORIENT Macro is a systematic Asian ETF strategy by One Altitude Capital using US macro regime signals. Backtest 2022–2025: +73.4% total return vs +34.1% EM Asia benchmark. BVI licensed. Minimum USD 250,000.

Godfried Meindertsma

1/6/20264 min read

ORIENT Macro Strategy — Systematic Asian Investing for the Real World

Most investors who want Asian market exposure face the same problem. Asian equity markets are volatile, driven by forces that are difficult to predict — Chinese regulatory risk, regional geopolitics, currency fluctuations and the ever-changing sentiment toward emerging markets. The standard solution is a broad Asian or emerging market ETF. The problem is that these funds are structurally constrained — they hold everything, including the parts of the market that are clearly in the wrong place at the wrong time.

ORIENT Macro takes a different approach.

Rather than holding a static basket of Asian equities, ORIENT Macro reads the current macro environment every week and rotates into the specific Asian ETFs best positioned to outperform in that environment. When global growth is strong and inflation is contained — Goldilocks — the strategy concentrates in Asian technology and semiconductor ETFs that benefit from US tech cycle momentum. When commodities and inflation are rising — Reflation — it shifts toward commodity-rich ASEAN markets. When growth slows and inflation remains elevated — Stagflation — it rotates entirely out of equities into precious metals and defensive positions, protecting capital while broad Asian indices suffer.

This is not market timing. It is regime awareness — reading the macro environment systematically and responding with discipline rather than emotion.

The signal architecture

ORIENT Macro uses the same nine US macro signals that drive the Atlas Macro strategy — credit spreads, equity momentum, yield curve shape, commodity prices, USD strength and more — to determine the prevailing regime. The decision to use US signals rather than Asian signals reflects a clear empirical reality: US monetary conditions and technology sector momentum are the primary drivers of risk appetite for Asian markets, regardless of what regional central banks are doing.

Within the confirmed regime, the strategy selects from a curated universe of Asian and global ETFs, choosing the top performers by accelerated momentum — a combined 1-month, 3-month and 6-month return signal that identifies sustained trend strength rather than short-term noise.

A semiconductor momentum override can concentrate the portfolio in Korean and Taiwanese semiconductor ETFs when tech cycle momentum is exceptional — capturing the kind of leadership that broad EM indices miss because of their significant China allocation.

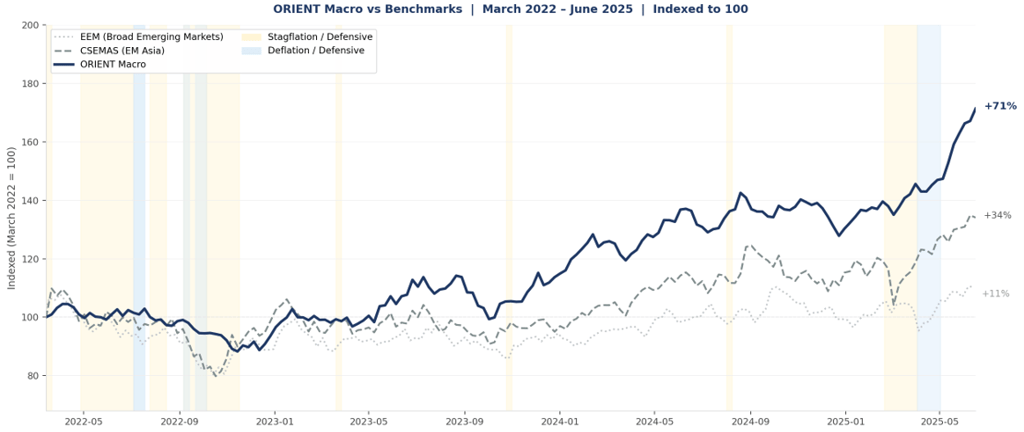

What the backtest shows

A historical simulation covering March 2022 through June 2025 — encompassing the global inflation shock, the 2022 bear market, the 2023-2024 technology-led recovery and the 2025 tariff-driven volatility episode — produced a total return of +73.4% against +34.1% for the iShares MSCI EM Asia ETF and +10.7% for the iShares MSCI Emerging Markets ETF over the same period.

The outperformance came from two sources. During the 2022 stagflation episode and the 2025 tariff shock, the strategy rotated entirely out of Asian equity into managed futures, market-neutral positions and short-duration bonds — while the EM Asia benchmark fell over 40% peak to trough. And during the 2023-2024 AI cycle, the semiconductor override captured gains that broad indices missed. The strategy protected on the way down and participated fully on the way up.

Current status

ORIENT Macro is currently live in a trading phase, accumulating signal history and execution experience. The planned agentic AI risk management layer — already operational in the APEX Momentum strategy — will be added once sufficient live track record has been established.

The strategy is available to accredited investors with a minimum allocation of USD 250,000, either as a standalone mandate or as part of the broader APEX platform alongside Atlas Macro, APEX Momentum and Quantamental Momentum.

To receive the full ORIENT Macro strategy document or discuss allocation, contact One Altitude Capital directly.

Strategy mechanics — how the regime detection works

The regime engine monitors nine market signals weekly, scoring each for direction and magnitude. Growth signals include SPY momentum, HYG/IEF credit spread and XLB materials momentum. Inflation signals include GLD gold momentum, XLE energy momentum and UUP dollar strength. A yield curve signal and hysteresis band prevent false regime switches from short-term noise.

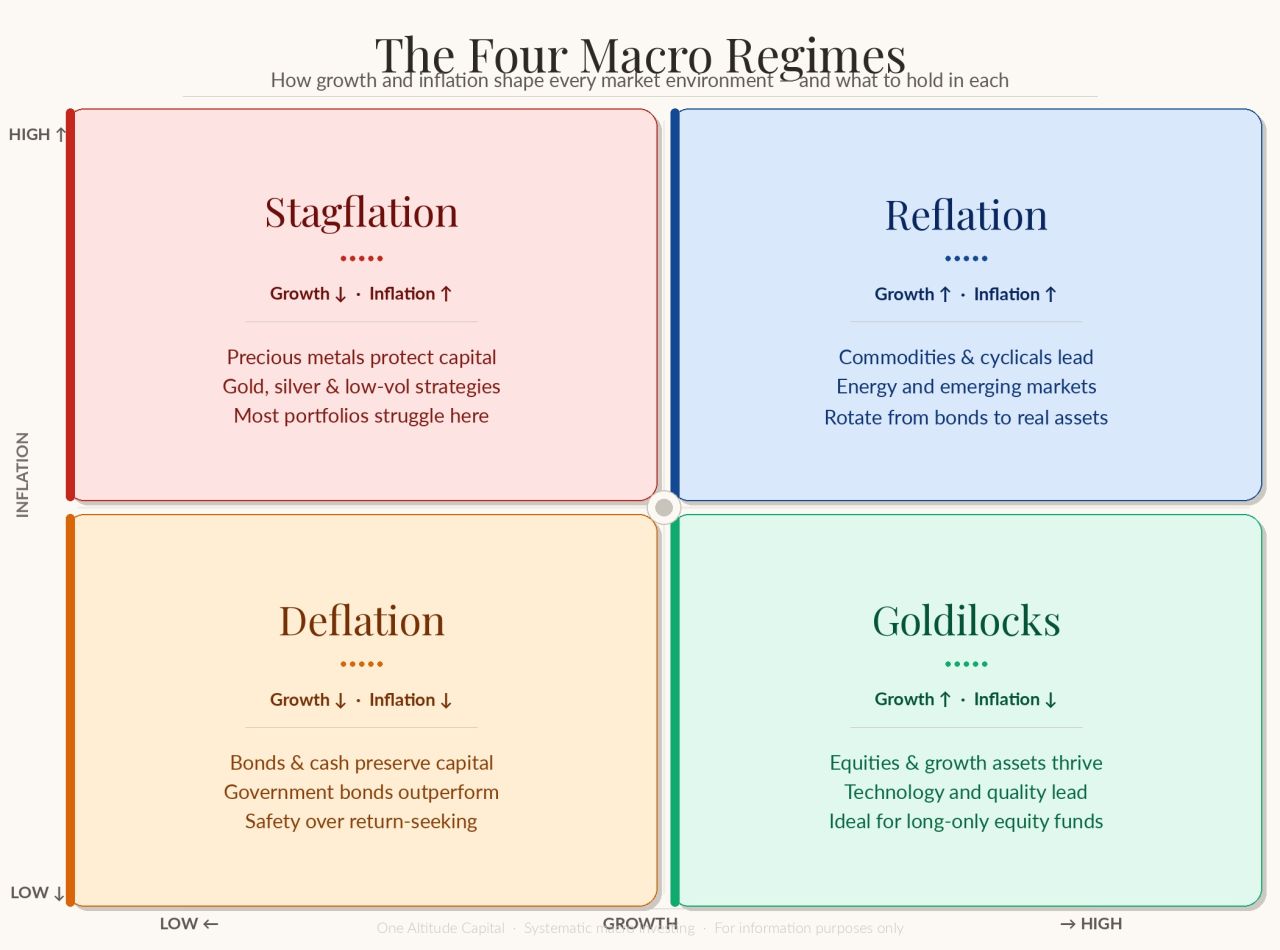

The four regimes and their ORIENT Macro universe:

Goldilocks — Growth ↑ · Inflation ↓

Asian technology and semiconductor ETFs. Korean and Taiwanese market leaders benefit directly from US tech cycle leadership. SMH semiconductor override activates when tech momentum exceeds threshold.

Reflation — Growth ↑ · Inflation ↑

Commodity-rich ASEAN markets. Energy, materials and emerging market ETFs with high commodity exposure outperform as global demand and inflation rise simultaneously.

Stagflation — Growth ↓ · Inflation ↑

Precious metals and defensive positions. GLD, SLV, managed futures and market-neutral ETFs replace equity exposure entirely — the regime where most Asian equity funds suffer their worst drawdowns.

Deflation — Growth ↓ · Inflation ↓

Short-duration bonds and cash equivalents. Capital preservation takes priority as both growth and inflation contract.

Selection methodology

Within the confirmed regime universe, the strategy ranks all eligible ETFs by accelerated momentum — a combined 1-month, 3-month and 6-month return signal. The single highest-ranked ETF is selected for the full week's allocation. An absolute momentum filter requires a positive 6-month return before any ETF qualifies for entry — routing the portfolio to cash when no ETF passes the filter.

Regime changes are subject to a two-period confirmation lag to prevent whipsawing on temporary signal noise. The full rebalance executes every Monday at 11:00 CET via IBKR Adaptive algorithm.

Backtest performance summary

MetricORIENT MacroEM Asia BenchmarkEM BenchmarkTotal return+73.4%+34.1%+10.7%PeriodMar 2022 – Jun 2025SameSameSharpe ratio0.91——Max drawdown−12.5%−40%+−40%+

Backtest results are not indicative of future performance. Live trading commenced 2025. Walk-forward history accumulating.