Orient Macro strategy

Our Asian macro quant is live

1/6/20262 min read

The ORIENT Macro Strategy is a systematic, rules-based investment strategy that dynamically allocates capital across a curated universe of Asian and global ETFs in response to changing macroeconomic conditions. Anchored in the same four-regime framework that drives the ATLAS Macro Strategy, ORIENT Macro adapts the signal architecture for the Asian investment universe — rotating capital into the ETFs best positioned to outperform within the prevailing global macro environment.

The strategy uses US-based macroeconomic and market signals to determine regime, reflecting the demonstrated reality that US monetary conditions, credit spreads and technology sector momentum are the primary drivers of risk appetite for Asian equity markets regardless of regional central bank divergence. Within the confirmed regime, the top three ETFs by accelerated momentum are selected from a regime-specific candidate pool, with a momentum override mechanism capable of concentrating the portfolio in high-conviction technology positions when semiconductor momentum is exceptional.

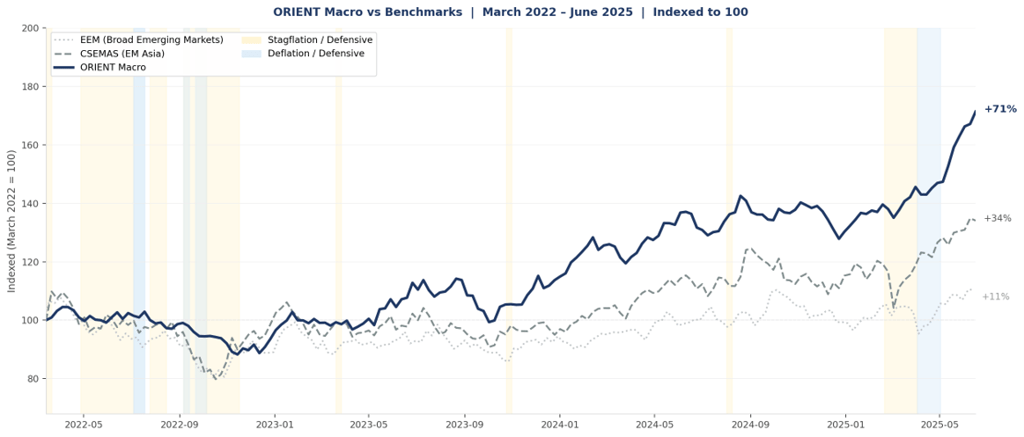

A historical simulation covering March 2022 through June 2025, encompassing the global inflation shock and rate hiking cycle, the 2022 bear market, the 2023-2024 technology-led recovery and the 2025 tariff-driven volatility episode, produced a total return of +73.4% against +34.1% for the iShares MSCI EM Asia ETF (CSEMAS) and +10.7% for the iShares MSCI Emerging Markets ETF (EEM) over the same period. The strategy is currently live in a trading phase, accumulating signal history and execution experience before deployment to investors.

The outperformance is attributable to two systematic sources. First, regime-driven capital protection: the strategy rotated out of Asian equity entirely during the 2022 stagflation episode and the 2025 tariff shock, holding managed futures (DBMF), market-neutral (BTAL) and short-duration bonds (SHY, GLD) while both benchmarks suffered significant drawdowns. EEM fell over 40% peak to trough in 2022 while the strategy remained near par. Second, concentrated technology selection: the SMH momentum override rotated the portfolio into Korean and Taiwanese semiconductor ETFs during the 2023-2024 AI cycle, capturing gains that broad EM indices missed due to their significant China allocation. The strategy has not yet deployed the planned agentic risk management layer, which is expected to further reduce drawdown during regime transitions.

Met

ORENT Macro

CSEMAS (EM Asia)