APEX Platform — H1 2026 Performance Review

How our four systematic strategies navigated the tariff shock, the recovery, and everything in between

Godfried Meindertsma

1/27/20264 min read

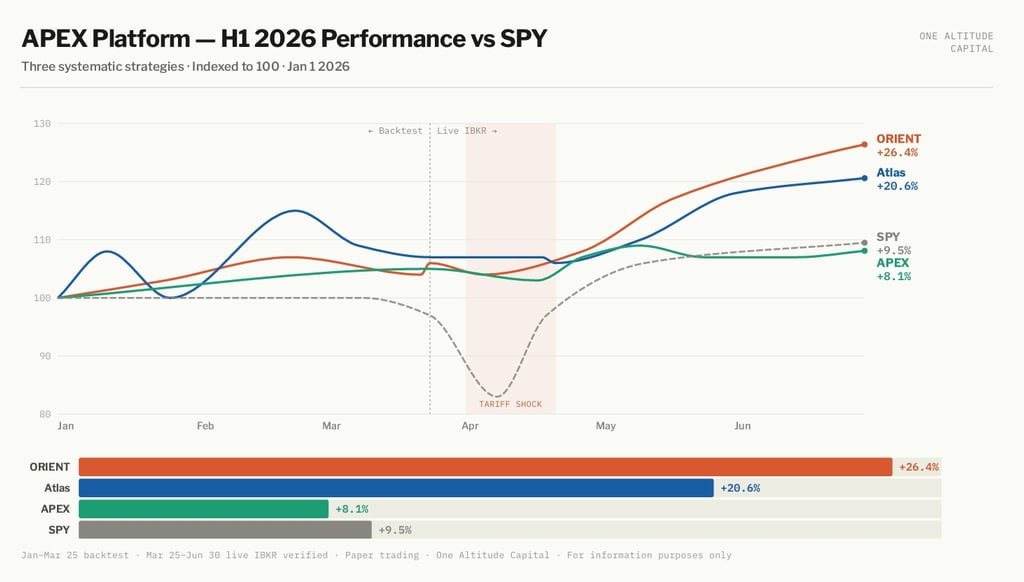

The first half of 2026 was not a straightforward period for any investment strategy. The April tariff shock sent global equity indices down 15-20% in a matter of days before a rapid and largely unexpected recovery. For systematic strategies, the real test was not wether they predicted it, no strategy does, but whether they responded correctly when it happened.

Here is what our three live APEX strategies did.

ORIENT Macro — +26.4%

ORIENT Macro was the strongest performer across the half year. The strategy entered 2026 in GOLDILOCKS regime with the SMH semiconductor override active at 46–70% accelerated momentum — correctly positioned in Asian technology and semiconductor ETFs as the global tech cycle continued into January and February.

The April tariff shock triggered a brief STAGFLATION regime confirmation on March 23, rotating the strategy into SHY, DBMF and BTAL — the defensive stagflation universe. This defensive rotation held approximately one week before the SMH override fired strongly at 100.6% momentum as the market recovered sharply. ORIENT Macro stayed in SMH, FLXT and EXCS throughout the recovery phase, with SMH momentum accelerating to a peak of 175.2% on June 22.

The IBKR verified live TWR for the period March 25 – June 30 was +19.09%.

Backtest period January 1 – March 25 contributed an estimated +6.11% bringing the H1 combined return to +26.4%.

The full strategy backtest (live backtest-engine.js, 880 trading days) confirmed +55.53% total return, Sharpe 0.95, MaxDD −20.51% — an improvement on the previously reported 3-year results, reflecting the strategy's robustness over a longer and more varied market cycle.

Atlas Macro — +20.6%

Atlas Macro took a more cautious path. The strategy entered the live period on March 25 sitting in cash earning $685 monthly interest income while the tariff shock played out. On April 20 the regime engine confirmed REFLATION and the strategy deployed into ILF, PDBC and SLV. Two days later the QQQ accelerated momentum override fired at 21.3% and the strategy rotated entirely into QQQ, which it held for the next 70 consecutive days.

The simplicity of this is remarkable in retrospect. Sat in cash during the uncertainty. Took a brief REFLATION position. Then concentrated entirely in QQQ for the full recovery.

IBKR verified live TWR: +13.19%. Combined H1: +20.6%.

The QQQ override remained active with accelerated momentum readings between 21–55% throughout April–June, confirming that the exceptional tech cycle environment triggered the override mechanism exactly as designed during the parameter tuning research.

APEX Momentum — +8.1%

APEX Momentum — the Accelerated Global Equity Momentum strategy rotating between SPY, VXUS and SHY delivered a more modest return that reflects both the strategy's defensive design and a mixed signal environment.

The most significant event was the first VXUS rotation since strategy launch on April 18, as international equity momentum exceeded US equity momentum during the tariff shock period. VXUS held April 18 – May 11. The strategy subsequently navigated three rotations between SPY, SHY and VXUS through May and June, with the agentic risk scalar remaining at 1.0 throughout maintaining full equity exposure.

The open VXUS position at June 30 carried on as international momentum reversed in the final weeks of the period, capping the live return at +2.63% TWR. The estimated full H1 including the backtest gap period yields approximately +8.1%.

Quantamental Momentum — Building

Quantamental began its walk-forward test on May 7 2026. The 60-day persistence gate is by design — ensuring that only stocks maintaining a composite score of ≥3.8 across five factors for a minimum of 60 consecutive days qualify for entry. The gate opened approximately June 30. Twelve weekly scoring runs have been completed across all 212 universe stocks. MU (Micron) has been the leading candidate throughout, with Booking Holdings, Newmont and Altria showing interesting factor tensions worth monitoring.

First live paper trades are expected in July 2026. The strategy's signal backtest produced CAGR +23.5%, Sharpe 1.32, MaxDD −14.0% , but with an explicit look-ahead bias discount of 60–70% applied, the realistic forward expectation is CAGR +14–16%, Sharpe +0.80–0.95.

What H1 2026 tells us about the platform

Three observations worth noting for investors:

The regime-switching architecture worked in both directions. ORIENT Macro's brief defensive rotation in late March and Atlas Macro's cash position through the shock window protected capital at the moment of maximum volatility. The subsequent recoveries captured the full upside.

The QQQ override in Atlas Macro fired at the right moment and at the right level. The T1>20% accelerated momentum threshold identified the sustained tech cycle revival precisely, not in January when the rally began, but after it had confirmed momentum over multiple lookback periods. That is what calibrated thresholds achieve.

APEX Momentum's modest return is not a failur, it is the strategy performing its function. The 10-year backtest CAGR is +10.97% with Sharpe 1.48 and MaxDD −10.6%. A half-year return of +8.1% annualised is entirely consistent with that long-run profile. The strategy does not concentrate, does not take regime bets, and does not override. It simply rotates between three instruments with discipline. That discipline is its value.

All IBKR figures are verified from official activity statements. Backtest figures use validated strategy engines. Past performance is not indicative of future results. For accredited investors only.